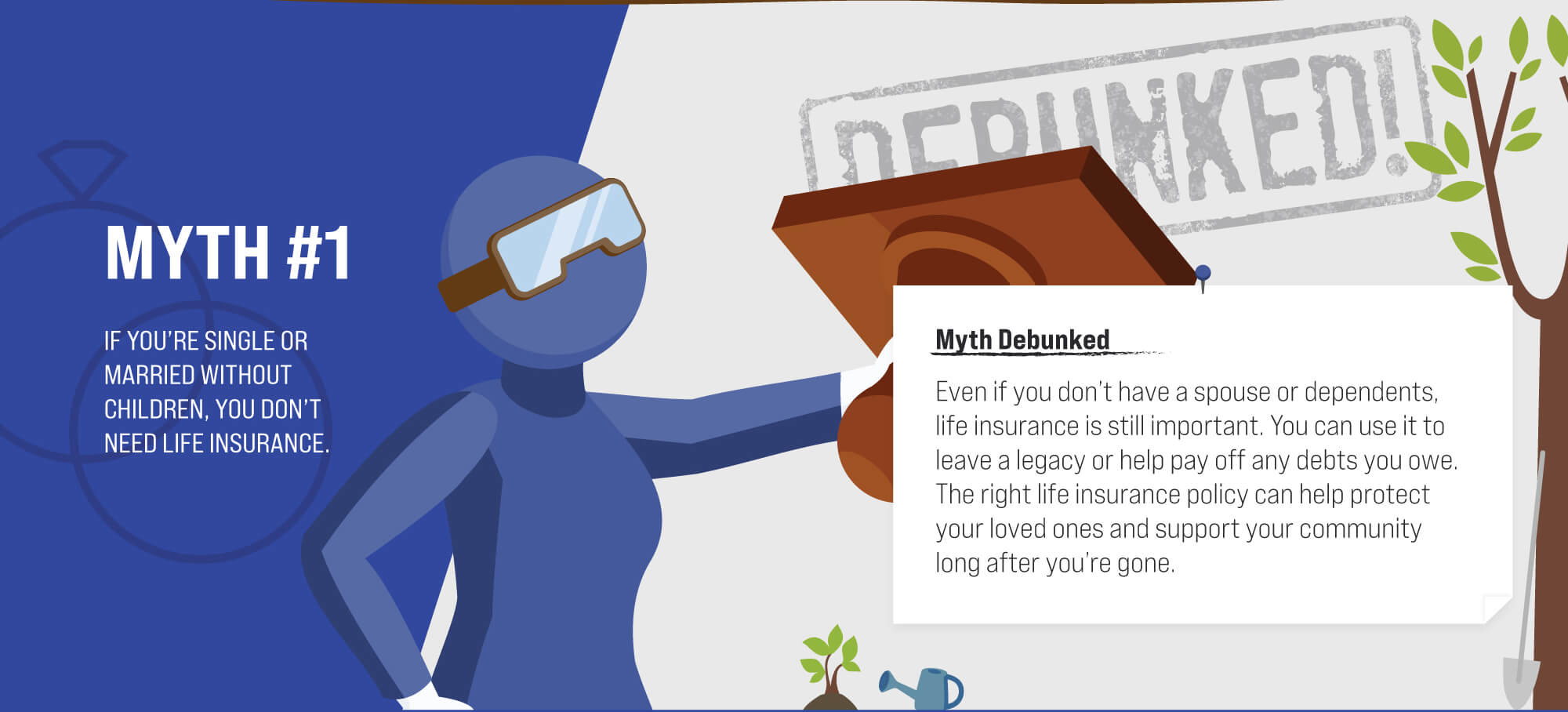

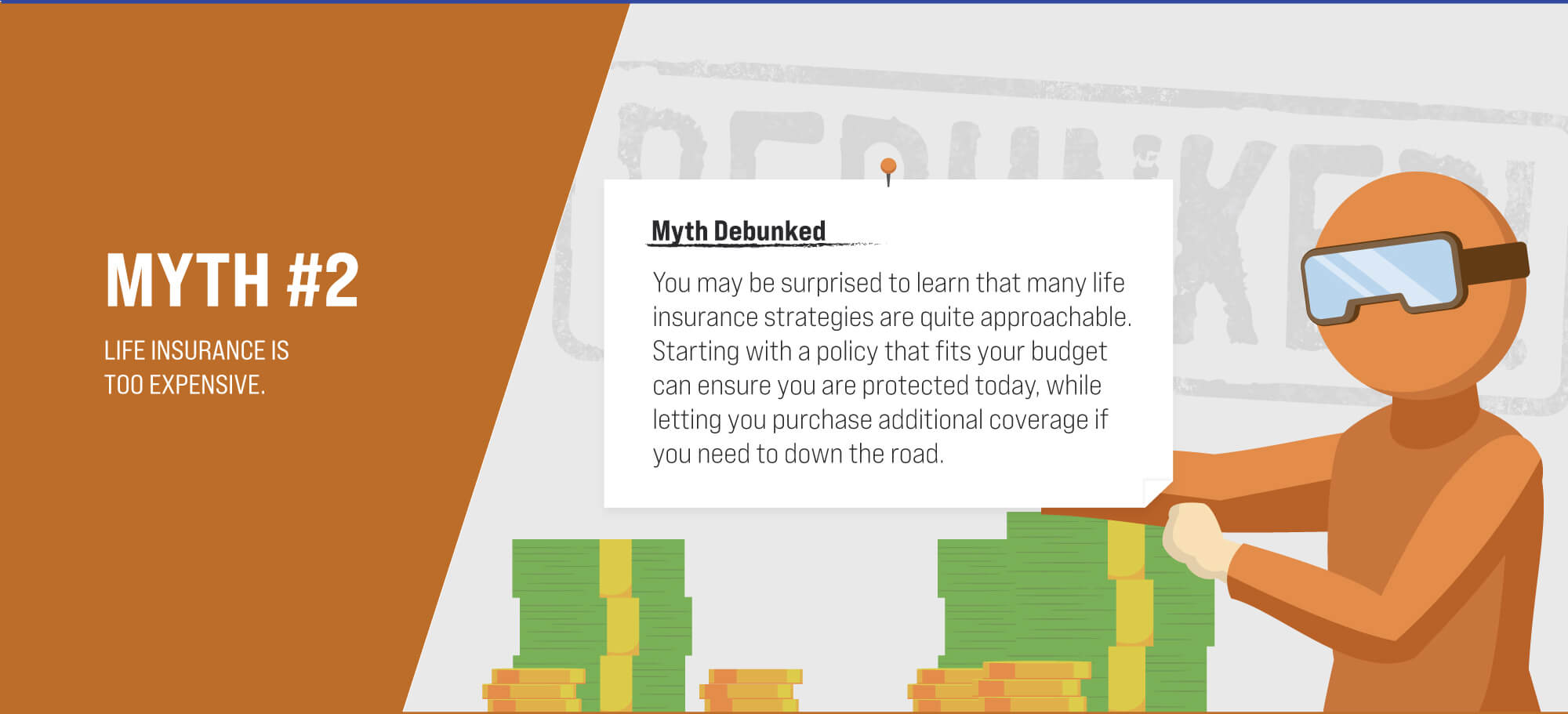

Life Insurance Myths: Debunked

This calculator can help you estimate how much you should be saving for college.

Coaches have helped you your whole life, in ways big and small. We'd like to be one of them.

Here are 5 reasons why you may consider working through retirement.